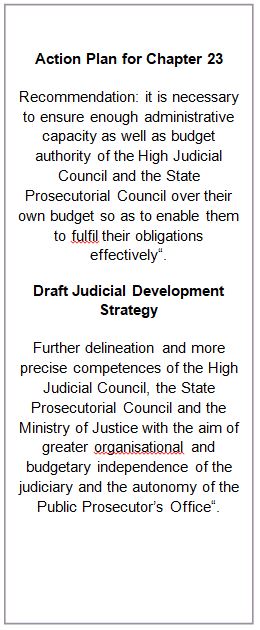

INTRODUCTION OF A NEW BUDGETING METHODOLOGY AS A PREREQUISITE FOR STRATEGIC PLANNING OF JUDICIARY PERFORMANCE

One of the Project’s terms of reference is the drawing up of a recommendation for a new budgeting methodology which would, among other things, contribute to greater independence of the judicial branch of the government, which entails an budget consistent with the desired performance of the judiciary. An objective budget is a budget which is aligned with the scope of planned work and adequate resources, established according to objective and transparent criteria (standards), and which enables the realisation of the planned performance of the judiciary.

The recommendation for a new budgeting methodology will lay out the following:

- Which concrete purposes the resources are spent for;

- How such spending is related to mid-term goals;

- What results are achieved.

The Project held a workshop in Novi Sad on December 7 and 8, 2018 together with the representatives of the Council, when, among other things, preliminary observations on the current state of organisation, competence and capacity of the Council and the Administrative Office were presented, as well as the goals, priorities, purpose and expected outcomes of the Project, one of which is the need to devise a new budgeting methodology.

The Project also pointed to the importance of introducing a modern process of mid-term budget planning, which has a clearly defined budgeting calendar and institutional division of accountability. Mid-term budget planning means that the budget is planned for a three-year period, i.e. an estimate of the annual budget for the following fiscal year and preliminary budget projections for another two fiscal years. The budget cycle has five stages: Planning, Programming, Budgeting, Execution and Reporting.